Too Little Too Late | Maybank Revamps AMEX Reserve for 2026

- May 10

- 11 min read

Updated: May 10

Let me start by saying that banks do not simply “revamp” a credit card proposition for no good reason, especially when the so-called revamp involves offering materially higher rewards and richer benefits.

So, one must wonder exactly how poor the performance of the Maybank 2 Cards Premier Reserve American Express has become for Maybank to suddenly turn around and offer more than double the Miles-Per-Ringgit in certain categories.

In the grand scheme of payment economics, this is an especially interesting move. Malaysia is not Singapore. Domestic interchange fees are capped, margins are tight, and banks are generally stingy when it comes to rewarding local credit card spend. That is precisely why most Malaysian airline miles cards either reward overseas spend aggressively, impose category restrictions, or hide behind complicated caps and exclusions.

Hence, Maybank’s decision to improve the AMEX Reserve is both refreshing and slightly suspicious.

Spoiler alert: this is a decent revamp. In isolation, the upgraded Maybank 2 Cards Premier Reserve American Express is now a much better card than before. But when you zoom out and compare it against the current Malaysian airline miles credit card landscape, it becomes painfully clear that the AMEX Reserve’s glory days are likely over.

The card is better, yes.

But the market has moved on.

Either way, let’s dive into what exactly has changed, what cardholders should expect when the revised benefits go live on 1 June 2026, and why Maybank’s renewed bet on AMEX may be inspiring, but ultimately still feels strategically questionable.

Maybank Introduces Dining MPR for AMEX Reserve

Let’s start with the biggest change.

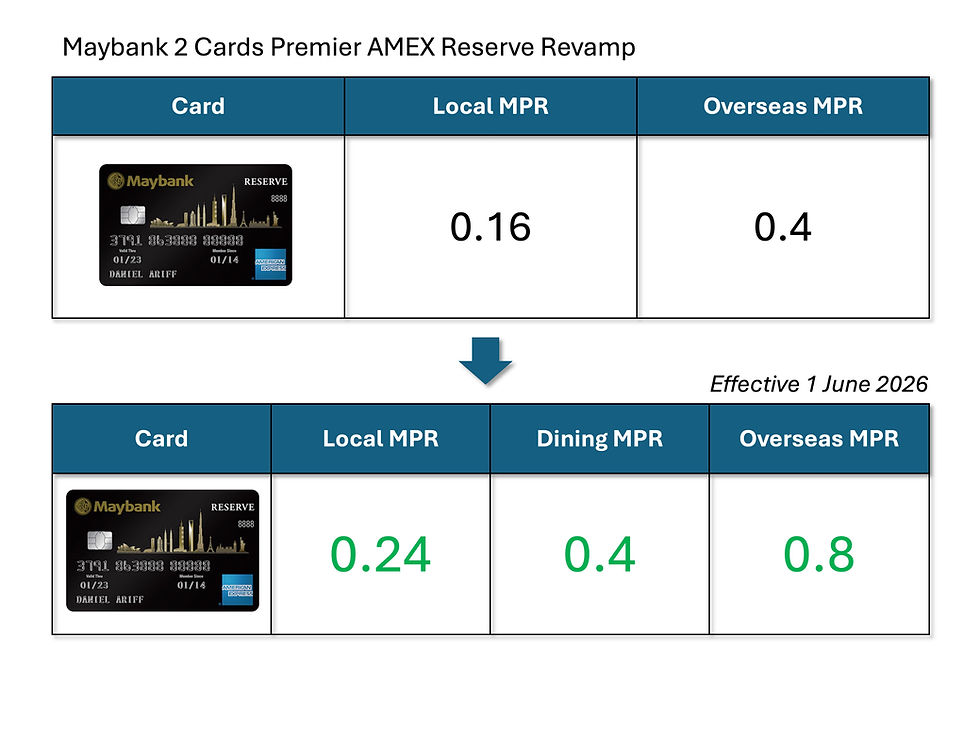

Effective 1 June 2026, the Maybank 2 Cards Premier Reserve American Express will offer 5X TreatsPoints on local dining spend, covering MCC 5811, 5812, 5813 and 5814. In plain English, this means caterers, restaurants, drinking places and fast food merchants.

Using Maybank’s current TreatsPoints to Air Miles conversion ratio of 12,500 TreatsPoints to 1,000 miles, 5X TreatsPoints translates into 0.4 Miles Per Ringgit.

That is a straightforward upgrade, and to be fair to Maybank, it is a meaningful one. Dining is one of the most important spending categories for affluent Malaysians, and any serious miles strategy should take dining spend into account. Everyone has to eat. The only question is whether your credit card rewards you properly for it.

However, once we compare this against the wider market, things start looking less exciting.

The CIMB Visa Infinite already offers 0.4 MPR on dining spend, and this can go up to 0.64 MPR if you hit the RM5,000 monthly spend threshold under CIMB’s ongoing bonus points structure. More importantly, the CIMB Visa Infinite only requires RM60,000 in annual income and carries zero annual fee. That alone makes Maybank’s proposition look less impressive.

Likewise, against competitors in a similar annual income range, the AMEX Reserve still struggles to stand out. The Standard Chartered Journey Mastercard offers 0.5 MPR on dining spend with no minimum spend requirement. The UOB Visa Infinite offers around 0.41 MPR on local dining with an easily achievable RM1,000 monthly dining spend requirement.

And of course, no discussion on dining-focused miles cards in Malaysia is complete without mentioning the Hong Leong Bank Visa Infinite, which currently offers an industry-leading 1 MPR on local dining, albeit with the caveat that you are locked into the Enrich Miles ecosystem.

This is the harsh truth. Maybank’s dining revamp is good, but competitors are already matching or exceeding it. In some cases, they are destroying it.

And then we arrive at the biggest deal-breaker of all: AMEX acceptance in Malaysia.

A 0.4 MPR dining rate is only useful if you can actually use the card. None of the competitors mentioned above suffer from the same acceptance issue as the Maybank 2 Cards Premier Reserve American Express. That alone tells you everything you need to know.

Maybank Boosts the AMEX Reserve’s Local and Overseas MPR Rates

Moving on to better news, the AMEX Reserve will now earn 3X TreatsPoints on other local spend, up from 2X, and 10X TreatsPoints on overseas spend, up from 5X. This is where the revamp becomes genuinely interesting.

At 10X TreatsPoints, overseas spend now translates into 0.8 MPR. That is a clear and meaningful upgrade, and it immediately places the AMEX Reserve back into the conversation for overseas spend.

To Maybank’s credit, 0.8 MPR is competitive. Against its closest competitor, the CIMB Travel World Mastercard, the AMEX Reserve now looks stronger on paper. The CIMB Travel World Mastercard earns around 0.64 MPR on Enrich Miles and around 0.53 MPR on other frequent flyer programmes, so Maybank clearly wins on raw overseas MPR.

For affluent Malaysians who are likely to convert bank points into Enrich Miles, KrisFlyer miles or Asia Miles, the AMEX Reserve finally becomes a serious overseas spend card again.

However, this is where we need to separate spreadsheet fantasy from real-world usability. AMEX acceptance abroad is better in some markets, especially the US. Singapore is generally more usable than Malaysia, particularly at hotels, restaurants and premium retailers. Europe, however, remains inconsistent. In some places, AMEX works beautifully. In others, you will be reaching for your Visa or Mastercard within five seconds. So while the 0.8 MPR overseas rate is attractive, it is not a clean win.

When benchmarked against UOB’s ecosystem, Maybank still has a problem. The UOB Visa Infinite and UOB PRVI Miles Elite both offer highly competitive overseas MPR rates, with the PRVI Miles Elite offering up to 1 MPR in selected ASEAN markets such as Singapore, Thailand, Indonesia and Vietnam. Crucially, both operate on Visa or Mastercard rails, which means cardholders do not need to worry as much about acceptance.

In other words, the AMEX Reserve has the rate. UOB has the usability. That is a very important distinction. More importantly, it's well known in the banking industry that AMEX charges you a higher FX fee (more so than Mastercard and Visa) when spending overseas, so expect to pay more in terms of cost per mile.

Now, looking at local spend, the AMEX Reserve’s new 3X TreatsPoints rate translates into 0.24 MPR. To me, this is actually the most objectively useful upgrade in the entire revamp. Why?

Because local general spend is where Malaysian banks are usually the most conservative. Overseas spend is easier to incentivise because banks earn more through FX fees and cross-border economics. Local spend is much harder to justify, especially when interchange is capped and rewards liability sits heavily on the bank’s books.

That is why most banks either offer miserable local earn rates or restrict meaningful earning to specific categories like dining, travel, groceries or online spend.

Against that backdrop, 0.24 MPR on general local spend is strong for a RM100,000 annual income card. It now places the AMEX Reserve among the stronger local general spend cards in Malaysia, behind only a small group of higher-tier of priority banking products such as the Hong Leong Bank Visa Infinite P and HSBC Premier Travel Mastercard.

This is a substantial upgrade, and I suspect this will be the main reason the AMEX Reserve sees better performance from 1 June 2026 onwards.

However, there are exclusions worth highlighting. The 10X overseas earn rate is not universal. Professional services and trading-related MCCs such as 6051, 6211 and 7311 will earn lower rates, with 2X TreatsPoints locally and 5X TreatsPoints overseas. What remains unchanged is that utilities, education, EzyPay and insurance transactions will only earn 1X TreatsPoints. Meanwhile, MyCCDD, government bodies, JomPay, FPX and e-wallet reloads will earn no TreatsPoints at all.

Still, credit where credit is due. Maybank is now offering one of the strongest local general MPR rates available at the RM100,000 annual income level. That deserves recognition. But is it sustainable? That is the real question.

Because not too long ago, Maybank gave us the catastrophic TreatsPoints to Air Miles fiasco, where monthly airline miles redemptions were effectively capped and customers had to fight for redemptions using their own hard-earned points.

It was the credit card equivalent of Hunger Games, except instead of fighting for survival, people were fighting to convert their TreatsPoints before the monthly quota disappeared.

The reason was obvious: margins and profitability. So while this AMEX Reserve upgrade is positive, one must ask whether this is part of a proper long-term strategy, an incentive arrangement baked into the Maybank-American Express partnership, or simply Maybank deciding to be generous today before remembering profitability tomorrow.

Because if history has taught us anything, it is that Maybank is perfectly capable of launching something exciting, letting customers build their strategy around it, and then nuking the entire proposition from orbit.

A Huge Slap in the Face for Visa and Mastercard?

As Malaysia’s largest bank, Maybank makes some of the strangest decisions when it comes to credit cards, points and miles.

Putting aside the infamous TreatsPoints fiasco, the latest AMEX Reserve revamp is actually a huge slap in the face for Maybank’s own Visa and Mastercard portfolio.

Let’s start with the Maybank Visa Infinite.

The Maybank Visa Infinite is offered alongside the AMEX Reserve as part of the Maybank 2 Cards Premier package, and is also available as a standalone card. It has a similar annual income requirement, but now looks significantly weaker than its AMEX counterpart.

Sure, the Maybank Visa Infinite remains useful when you are swiping at merchants that do not accept AMEX. In fact, that is probably its main purpose now. But the difference in rewards is almost hilarious.

Why would a cardholder willingly use the Maybank Visa Infinite for eligible spend when the AMEX Reserve now earns more across key categories? The answer is simple: because the merchant does not accept AMEX. That is not a value proposition. That is a backup plan.

The situation becomes even more absurd when we look at the Maybank World Elite Mastercard, which is currently positioned as Maybank’s most affluent credit card. Despite its RM190,000 annual income requirement, the card continues to offer some of the worst MPR rates in the premium credit card space.

With the AMEX Reserve also offering benefits such as up to 50% off dining at Shangri-La Kuala Lumpur and up to 40% off dining at Marriott hotels in Malaysia, what exactly is the selling point of the Maybank World Elite Mastercard?

But perhaps no Maybank customer should feel more forgotten than Maybank Diamanté Visa Infinite cardholders. Imagine placing millions in Assets Under Management with Maybank, only to realise that your credit card benefits are worse than cards available to customers with a RM60,000 or RM100,000 annual income requirement.

The scale of strategic incoherence is unbelievable.

The question remains: is Maybank deliberately favouring its American Express cards over its Visa and Mastercard counterparts?

Looking at the broader portfolio, the answer appears to be yes. The KrisFlyer AMEX Platinum remains relevant in the local miles space. The Maybank Platinum Charge Card still has a role for high-spending AMEX users. And now, the AMEX Reserve has received a surprisingly meaningful revamp.

Meanwhile, the Visa Infinite looks increasingly like an afterthought, the World Elite Mastercard feels badly outclassed, and Diamanté customers continue to receive a proposition that does not reflect the level of wealth relationship required.

For a bank of Maybank’s size, this is not just strange. It is borderline comedic.

AMEX Acceptance in Malaysia

No AMEX-related article is complete without talking about the elephant in the room: American Express acceptance in Malaysia.

American Express itself states that it has more than 130,000 merchant locations in Malaysia. On paper, that sounds decent. In reality, anyone who has seriously tried using AMEX as a daily driver in Malaysia knows the experience is nowhere close to Visa or Mastercard.

That is the core problem with any AMEX-based miles strategy. The headline MPR may look attractive, but the realistic MPR depends on where you can actually spend. If you constantly need to ask “Do you accept AMEX?” before paying, the card is not truly a universal daily driver. It is a selective-use card.

This is especially true outside affluent urban pockets. In areas like Bangsar, Mont Kiara, KLCC, Pavilion, Damansara Heights and selected premium retail or hotel environments, AMEX acceptance can be decent. At higher-end restaurants, luxury retailers, hotels and selected grocery chains, you may get lucky. But once you move into broader everyday spending, acceptance becomes much more inconsistent.

And this matters because miles accumulation is not just about theoretical earn rates. It is about friction.

A great credit card should fit into your lifestyle. It should not force you to change where you eat, shop or spend just because you are desperate to earn miles.

I have said this before in my KrisFlyer AMEX Platinum article, and the same logic applies here: if you start paying more just to force an AMEX transaction, you are not optimising miles. You are lighting cash on fire and calling it strategy.

Malaysia’s payment landscape has also evolved massively. E-wallets, DuitNow QR and contactless payments are now deeply embedded into daily life. The issue is not whether Malaysians can pay digitally. We clearly can. The issue is whether American Express has enough acceptance breadth to compete with Visa and Mastercard in the places where Malaysians naturally spend.

And in that regard, AMEX still feels niche. This is why the AMEX Reserve revamp is both promising and flawed. The rewards are better. The proposition is sharper. But the acceptance issue remains the structural weakness that Maybank cannot simply ignore.

For existing cardholders who already spend heavily at AMEX-accepting merchants, this revamp is excellent news. You will earn more miles without changing much.

But for anyone considering the AMEX Reserve as a primary miles card, be careful. The real question is not whether 0.4 MPR on dining or 0.24 MPR on local spend is good. It is whether your actual spending pattern can meaningfully access those rates.

Because if half your merchants do not accept the card, the MPR exists only in theory.

Final Thoughts

The Maybank 2 Cards Premier Reserve American Express revamp is good. In fact, it is better than I expected.

The addition of 5X TreatsPoints on dining, the increase to 3X TreatsPoints on local spend, and the jump to 10X TreatsPoints on overseas spend make the AMEX Reserve a far more compelling card from 1 June 2026 onwards, at least if you put aside the higher AMEX FX charges.

For existing cardholders, this is a clear win. If you already know where AMEX is accepted and your lifestyle naturally fits within that ecosystem, the revised AMEX Reserve could become a very strong earning tool.

But for the wider Malaysian miles market, this feels like too little too late. The problem is not that the AMEX Reserve is bad. The problem is that competitors have already spent the last few years building stronger, more practical and more flexible propositions.

CIMB has built a broad ecosystem with strong merchant offers and multiple airline transfer partners. UOB has built one of the most practical miles ecosystems in Malaysia with fast points crediting and strong overseas spend mechanics. Hong Leong Bank has created an incredibly powerful Enrich-focused dining card. Standard Chartered has re-entered the premium conversation with stronger lifestyle and overseas propositions on its Beyond Visa Infinite.

Meanwhile, Maybank spent years letting its premium credit card ecosystem drift into mediocrity. Now, with this AMEX Reserve revamp, Maybank appears to be trying to reclaim relevance. That is admirable. It is even slightly exciting.

But it also feels unstrategic.

If Maybank is serious about winning back affluent miles chasers, it cannot rely solely on AMEX. Acceptance remains too limited, and the broader Visa and Mastercard portfolio is too weak. A strong AMEX card can be part of the strategy, but it cannot be the entire strategy.

That is why this revamp feels both inspiring and foolish. Inspiring, because Maybank is finally showing signs of life.

Foolish, because the bank appears to be placing its biggest upgrade on the payment network with the weakest acceptance in Malaysia, while leaving its Visa Infinite, World Elite Mastercard and Diamanté propositions looking painfully underwhelming.

The AMEX Reserve is now a better card, but better does not automatically mean best.

And unless Maybank fixes the rest of its premium credit card ecosystem, this revamp may end up being remembered not as a comeback, but as a desperate attempt to revive a card whose best days have already passed.

I have lost all my trust in Maybank's non-cobrand cards after Air miles fiasco. They seem to hold their customers in such contempt that they believe these frequent bait and switch tactics acceptable. I am sure Maybank will pull a fast one and deval the conversion in a couple months after they get a few sign-ups.

My wallet is now the CIMB Visa infintite, Krisflyer Amex, and a Chase Saphhire Preferred for when a retailer doesn't take QR or Amex.

A suggestion which you are free to ignore, it would be useful if you could add the AmBank VI and equvalent KrisFlyer cards to these tables so we can remind ourselves how these rates compare to commonly held Air Miles specific cards.

I am too lazy to have multiple cards, swapping out between shopping cateogories, etc. and want a one leg kick all card and at the moment AmBank is obvious choice because of the MAS benefit, even if points suffer a bit. How much I suffer I also don't know.

no friggin way im going back to maybank after all the crazy amount of time I spent trying to redeem my miles 😂

Good write up, still a very lousy card tbh