First Look | Standard Chartered Beyond Visa Infinite Malaysia

- Feb 4

- 13 min read

Updated: Feb 6

The official product page for the Standard Chartered Beyond Visa Infinite is up, so that's my green light for this article to go up.

“As the medieval chroniclers loved to warn: Fortune turns her wheel without apology. The fallen rise, and the comfortable tumble.”

If Standard Chartered Malaysia is attempting a comeback story in the premium credit card space, this is exactly the sort of moment it would pick: quiet, deliberate, and aimed squarely at the people who already live inside its wealth ecosystem.

Because once upon a time, the Standard Chartered Priority Banking Visa Infinite was the card that quietly signalled you were “in the club”. It wasn’t flashy. It didn’t need to be.

Standard Chartered’s strategy has always leaned heavily into affluent and wealth banking, where the real business isn’t interchange or points liability, but Assets Under Management (AUM), long-term client retention, and the ability to cross-sell a full suite of banking, investments, financing, and insurance solutions under one roof.

In that model, a premium credit card is less of a standalone product and more of a relationship anchor. It keeps the client transacting, keeps the bank top-of-mind, and gives Standard Chartered a practical touchpoint to reward behaviour that strengthens the banking relationship: deposits parked, investments held, wealth products adopted, and a broader share of wallet captured.

In short, the card isn’t the “end product”. It’s a sticky lever that makes the entire Priority Banking proposition feel tangible in day-to-day life.

But in the last decade, the Malaysian airline miles market moved on without Standard Chartered.

With the rise (and fall) of Maybank’s credit card ecosystem, and then the more aggressive premium playbooks from CIMB, RHB, and UOB, the SCB Priority Banking Visa Infinite slowly slid into irrelevance for anyone serious about miles. The card ended up being used less as a premium travel tool, and more as a dining cashback weapon for people who wanted perks… as long as those perks were cheap, simple, and immediately redeemable.

And that brings us to the most ridiculous chapter of all: Standard Chartered’s long-running dining cashback promo.

If you know, you know. Selected restaurants, cashback rewards, and a “first-come-first-served” pool that vanished faster than concert tickets. The best part? There was practically no meaningful real-time communication on whether the pool was already depleted. So you’d spend, pay, hope, and then wait like you just entered a raffle. It genuinely felt like Hunger Games: Malaysia Edition, except the prize was not dying, but getting your cashback.

Imagine having hundreds of thousands in AUM with a wealth bank, and still needing to treat dinner as a lottery ticket. That isn’t premium. That’s behavioural economics done badly.

Which is why the launch of the Standard Chartered Beyond Visa Infinite feels like a genuine turning point. This is Standard Chartered finally going “all-in” again, with a product that tries to be relevant to how affluent Malaysians actually spend: overseas, on dining, shopping, and experiences.

So, without further ado, let's dive in.

The Duality of Man

The Beyond Visa Infinite is not really a single credit card. It’s a two-tier strategy packaged under one name, and it only makes sense if you view it through Standard Chartered’s relationship-banking lens.

Most of the proposition is tied to your AUM relationship with Standard Chartered Malaysia, which means the “card benefits” are really a reflection of the banking tier you sit in.

To keep things clean, I’m going to treat them as two separate products:

Standard Chartered Beyond Visa Infinite

AUM requirement: RM350,000

Annual fee: RM800 (RM400 supplementary)

Standard Chartered Beyond Visa Infinite Priority Private

AUM requirement: RM3,000,000

Annual fee: RM2,000 (RM600 supplementary)

Made out of Metal (wooooo)

Standard Chartered has indicated the first-year annual fee will be waived, and I would not be surprised if future waivers are possible depending on the strength of your banking relationship. That’s consistent with how wealth banks operate: the “fee” is often a soft lever, not a hard rule, especially when AUM profitability is the main game.

The two cards have vastly different value propositions, and by the end of this article, I’ll tell you plainly which one I think is actually worth pursuing.

Airline Miles Earning Rates

Refined Points is, at its core, an airline miles blog. So we start with the only thing that truly matters: Miles per Ringgit (MPR).

Here are the earn rates as communicated for the Standard Chartered Beyond Visa Infinite Malaysia cards:

The logic is simple and, frankly, refreshing: the higher your AUM tier, the higher your overseas MPR. It’s a clean value exchange that doesn’t require a PhD in bank reward mechanics to understand.

Now, the elephant in the room: local spend.

Both versions of the Beyond Visa Infinite offer no meaningful local spend accelerators. No local dining boost. No groceries boost. No “everyday Malaysia” category that acknowledges the reality that most people… live in Malaysia.

That omission is a surprising choice, especially when competitors in a similar affluent tier do offer local dining accelerators. Not to mention, it's likely that the bulk of Standard Chartered Malaysia's customer base are Gen Xs whom spend most of their time in Malaysia.

Even if you argue that Malaysia’s domestic interchange economics are unattractive, that’s not a customer problem. That’s a product design problem. If you’re charging RM800 to RM2,000 a year, “we didn’t feel like subsidising local earn rates” is not exactly a premium narrative.

And it gets messier when you consider the points ecosystem.

It’s crucial to understand that the Beyond Visa Infinite earns 360 Rewards Points, while the Standard Chartered Journey Mastercard earns Airmiles Points. These are not the same bucket.

That means if you try to “patch” Standard Chartered’s weak local earn rate by pairing the Beyond Visa Infinite with the Journey Mastercard, you may end up creating a stranded points situation where you’re splitting spend across two incompatible reward currencies.

Anyone who lived through RHB’s Loyalty vs LoyaltyPlus nonsense will immediately understand why this is annoying, although I'll give Standard Chartered the benefit of doubt here, given that the minimum conversion threshold for the SC Journey is relatively on the low side.

Nevertheless, unless Standard Chartered is genuinely designing this card for customers who live permanently on airplanes, the absence of any meaningful local spend accelerator is difficult to defend.

This feels far less like a carefully considered strategic decision and far more like an aggressive cost-containment exercise dressed up as product design. One can almost picture an internal slide concluding that Malaysia’s low domestic interchange “doesn’t justify” rewarding local spend—an argument that may make sense in a spreadsheet, but collapses entirely when translated into a RM800–RM2,000-per-year consumer proposition.

At this level, the omission is not clever optimisation; it is product laziness. And for a card positioning itself as a flagship for affluent clients, that disconnect is glaring.

Now let’s talk about where this card actually shines: overseas.

When stacked up against competitors in both AUM and non-AUM distinctions, you'll find that the new Standard Chartered Beyond Visa Infinite(s) actually compare decently well. For avoidance of doubt, all MPR calculations below are on KrisFlyer/Asia Miles because no sane Malaysian in this level of affluence would convert points to Enrich!

The “overseas dining and shopping” accelerator is the right move, because a huge chunk of affluent overseas spend naturally falls under those two categories anyway.

You’ll still earn miles on things like train tickets, convenience stores, and random miscellaneous spend, but those will generally sit outside dining/shopping and earn at the base overseas rate.

Here’s a real-world example.

On a recent Japan trip, I spent around RM20,000 (no judgement please). Roughly:

40% travel-related (airlines, hotels, travel agencies)

35% shopping

15% dining

10% miscellaneous (convenience stores, transport, small-ticket items)

On my UOB PRVI Miles Elite, that trip earned me roughly 16,600 miles.

If I ran the exact same spend on the Standard Chartered Beyond Visa Infinite:

Dining + shopping (RM10,000) at 1.42 MPR = 14,200 miles

Everything else (RM10,000) at 0.71 MPR = 7,100 miles

Total = 21,300 miles

That’s roughly 20% to 25% more miles than what I earned previously, without changing spending behaviour. And that is exactly why the Beyond Visa Infinite has a legitimate place in the conversation: it rewards the spend pattern that affluent Malaysians actually have when travelling.

And yes, some would say it isn't a fair comparison between a RM100K annual income credit card and a RM350K AUM credit card, but I beg to differ, given that UOB's airline miles proposition has been decent as of late, and is a primary overseas spend card for many Refined Points readers.

I've added a chart here comparing how many miles you'll earn with RM20,000 overseas spend in Japan across major cards in the market for KrisFlyer/Asia Miles. Like I mentioned previously, no sane Malaysian in this level of affluence would convert points to Enrich, and hence that comparison is futile at best.

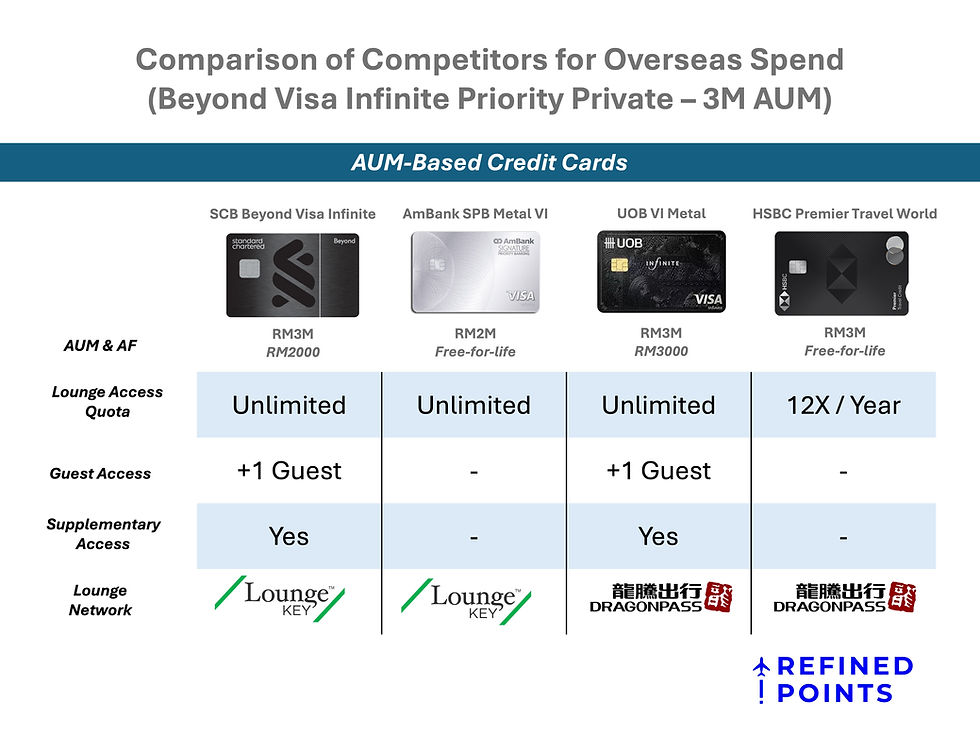

Airport Lounge Access

Malaysians love lounge access. Banks know this. Which is why Standard Chartered’s lounge proposition here feels oddly underwhelming.

Standard Chartered Beyond Visa Infinite

8x lounge access per calendar year

Important: the quota is shared between principal and supplementary cardholders (8 visits total, not 8 per card)

Standard Chartered Beyond Visa Infinite Priority Private

Unlimited lounge access for principal and supplementary cardholders

Principal cardholder can bring 1 guest

In today’s premium card landscape, 8x annual lounge access is simply not exciting, especially when you’re attaching both an AUM requirement and an annual fee to it.

Yes, unlimited lounge access is nice, but even that is no longer a differentiator. The UOB Visa Infinite Metal already offers a similar “unlimited” positioning, and several other cards offer generous access without demanding a RM3 million relationship.

I'll give credit where it's due: the Beyond Visa Infinite Priority Private does have pretty decent lounge access, but the UOB Visa Infinite Metal edges it slightly due to the gimmicky UOB Private Lounge (hey, a gimmick is still better than nothing!).

And then there’s the bigger issue: LoungeKey isn’t premium anymore. It’s functional, but it’s not aspirational. Pay-per-use lounges globally are packed to the brim, and the experience often ranges from “fine” to “why am I here”.

Take the Club Aspire Lounge at London Heathrow Terminal 5 as a classic example: industrial trays of reheated sausages, mass-produced scrambled eggs that taste like they were poured from a carton, and enough baked beans to feed a small medieval army. It’s less “luxury escape” and more “airport cafeteria with softer lighting”.

So when CIMB and Maybank can offer Plaza Premium First access (a far more premium lounge experience in many markets) without any AUM commitment, you have to ask the obvious question:

What exactly is Standard Chartered trying to achieve with this lounge strategy?

If Standard Chartered wanted to make a real statement, it would explore access to airline lounges in key global wealth hubs. Give me Cathay Pacific lounge access in Hong Kong as a Beyond Visa Infinite cardholder, and you’ve instantly created a premium proposition that affluent customers actually feel. Lower footfall, higher perceived value, and a far stronger story than “here are 1,500 LoungeKey lounges you’ll fight crowds in”.

Complimentary Airport Transfer

Both versions of the Beyond Visa Infinite come with complimentary Grab rides:

Beyond Visa Infinite: up to RM60 per ride, 6 redemptions per year (RM360 total value)

Beyond Visa Infinite Priority Private: up to RM100 per ride, 6 redemptions per year (RM600 total value)

Airport transfer perks are not common in Malaysia, so any inclusion is welcomed. But the value here is… awkward.

For comparison:

UOB PRVI Miles Elite: 2x RM80 Grab rides per month (up to 24 a year, RM1,920 value if fully utilised)

UOB Zenith World Elite: 2x RM180 Grab rides per month (up to 24 a year, RM4,320 value if fully utilised)

Even CIMB’s Travel Platinum Mastercard (a mass market card) offers a meaningful Grab voucher mechanic with a reasonable spend trigger.

So if a mass market card can offer a stronger annual Grab value proposition than a RM350K AUM premium card with an annual fee, something doesn’t add up.

I understand the angle: Standard Chartered is prioritising simplicity and predictability, not necessarily the highest possible value. But given the stakes of the Beyond Visa Infinite proposition, this benefit feels like it was designed by someone who doesn’t personally use airport transfers enough to realise what “good” looks like.

The Brilliant Dining Program

This is where the Beyond Visa Infinite finally starts to look dangerous, in a good way.

Standard Chartered appears to have moved away from the chaotic first-come-first-served dining cashback nonsense, and replaced it with a dining proposition that is far more aligned with how affluent customers actually spend.

Standard Chartered Beyond Visa Infinite

Up to 60% cashback at selected restaurants (including Michelin Guide venues)

Up to RM300 cashback per month

Standard Chartered Beyond Visa Infinite Priority Private

60% cashback at selected restaurants (including Michelin Guide venues)

Up to RM600 cashback per month

The “up to” wording matters, and we should not pretend it doesn’t. But assuming the mechanics are structured sensibly, this is easily the strongest lifestyle benefit in the Beyond Visa Infinite proposition.

If maxed out:

Beyond Visa Infinite: RM300 x 12 = RM3,600 annual value

Beyond Visa Infinite Priority Private: RM600 x 12 = RM7,200 annual value

That is serious money, and more importantly, it’s value that affluent customers can extract without needing to play Hunger Games with a cashback pool.

Also, Michelin Guide coverage in Malaysia is not small. The Michelin Guide Kuala Lumpur & Penang 2026 selection alone features 151 establishments across Michelin Star, Bib Gourmand, and Michelin Selected categories. If Standard Chartered’s participating list is even moderately broad, this benefit becomes genuinely usable.

Of course, the real question is the restaurant list. Based on the initial publicised list here, it appears that the programme covers a solid range of Michelin restaurants, hotel dining, and even several high-street restaurants such as Dragon-i.

Either way, this dining program is the highlight of the Beyond Visa Infinite Malaysia launch. Full stop.

Complimentary Business Class Upgrade Benefit for Priority Private

This is the one benefit I was hoping would not make it to Malaysia.

The Standard Chartered Beyond Visa Infinite Priority Private includes a once-per-year “complimentary business class upgrade” benefit, structured as follows (based on the current launch communication):

Buy 1 business class ticket + buy 1 economy class ticket (typically the most expensive Flex fare) on Malaysia Airlines

Receive 1 complimentary upgrade from economy to business class

Valid for routes within Asia once per year

I will keep this section short, because I’ve prepared a separate deep dive on the mathematics and probability of this perk.

But the core issue is simple: when an “upgrade benefit” forces you into the most expensive economy fare bucket, you often end up paying so much that the upgrade starts to look like a marketing trick rather than real value. And when you restrict it to Malaysia Airlines, in a region where a large portion of routes are operated by narrowbody aircraft with mediocre “business class” seats, you’re effectively asking your most valuable clients to get excited about an experience that many affluent Malaysians actively avoid.

This is not me being a Malaysia Airlines hater (even though I am). This is a value argument.

Priority Private clients with RM3 million AUM do not need a gimmick. They need a clean, premium, globally relevant benefit. This isn’t it.

Final Thoughts

After stepping back and looking at the Standard Chartered Beyond Visa Infinite holistically, one thing becomes increasingly clear: this card does not feel like the product of a single, unified vision.

Instead, it reads as though two very different teams were involved in shaping the value proposition—one that deeply understands affluent behaviour, and another that is still trapped in the comfort of legacy marketing tropes.

On one hand, there are genuinely excellent decisions. The complete removal of the first-come-first-served dining cashback “hunger games” is long overdue, and replacing it with a structured, predictable, and highly lucrative dining programme is exactly the kind of correction Standard Chartered needed to make. Likewise, the overseas dine-and-shop accelerator is intelligently designed and grounded in real spending behaviour. These are features that reward how affluent Malaysians actually spend when they travel, without forcing artificial behaviour or convoluted mechanics.

On the other hand, there are elements that feel entirely unnecessary—and worse, misaligned with the audience this card is supposedly built for. The complimentary Business Class upgrade benefit is the most obvious example. It is a headline-grabbing perk that sounds impressive in a brochure, yet quickly unravels once you examine the mechanics, restrictions, and real-world usability. This is not thoughtful value creation; it is benefit theatre.

And that is where the disconnect lies.

Standard Chartered’s most affluent clientele represent the very top of the affluent spectrum in Malaysia. This is a customer base built on generational wealth, serious entrepreneurs, senior executives, and globally mobile individuals who are deeply familiar with premium travel, airline products, and financial optimisation. These are not customers who need to be dazzled by gimmicks, nor are they swayed by artificially inflated “complimentary” benefits that fail basic value tests.

They understand value. They recognise substance. And they can immediately tell the difference between a well-designed benefit and a marketing distraction.

When the Beyond Visa Infinite leans into mechanics that are rational, transparent, and aligned with real spending—such as its overseas earn structure and revamped dining programme—it looks strong. When it strays into theatrical perks that add complexity without meaningful upside, it risks undermining the credibility of an otherwise promising product.

The irony is that Standard Chartered does not need to resort to these tactics. Its strength has always been its affluent franchise, its wealth banking depth, and the sophistication of its client base. The best version of the Beyond Visa Infinite is the one that respects that intelligence, not one that tries to impress it with noise.

At this point, my view is straightforward. The Beyond Visa Infinite Priority Private tier is not compelling enough to justify parking RM3 million in AUM purely for incremental perks, especially when one of the headline differentiators is a once-a-year Business Class upgrade that is inherently restrictive and, in practice, feels more like benefit theatre than real value. If you already sit in Priority Private territory then sure, you’ll enjoy the upsides, but using this card as the reason to “move up” a tier is not a rational financial decision for most people.

The RM350,000 AUM Beyond Visa Infinite, on the other hand, is the only version I’d seriously consider as a standalone proposition. The revamped dining programme is genuinely strong, it’s easy to understand, and it delivers tangible value without forcing you into complicated mechanics. The overseas dine-and-shop accelerator is also well designed and can outperform the usual miles-earning suspects when your spending profile matches the categories.

That said, it is still not a complete card. The lack of meaningful local spend accelerators is a glaring omission, and it leaves the Beyond Visa Infinite lagging behind competitors like the CIMB Preferred Visa Infinite and UOB Privilege Banking Visa Infinite for day-to-day Malaysia spend, particularly in categories like dining.

So the verdict is this: Priority Private is a nice-to-have if you’re already there, but not worth chasing. The RM350K tier can be good, but only when paired with the right local spend card, and only if you actually intend to extract value from the dining and overseas categories where this card is clearly engineered to shine.

As it stands, the Beyond Visa Infinite shows flashes of genuine brilliance—but also moments of unnecessary excess. Whether Standard Chartered chooses to refine this into a truly world-class premium card, or dilute it with further gimmicks, will ultimately determine whether this comeback story reaches its full potential.

UOB PME has DragonPass?

The annual fee can be waived if the relevant AUM is maintained. It is on the website

Feels like a visa infinite and nothing really beyond

Brilliantly written👍