Gone and Forgotten: The Alliance Bank Visa Infinite

- Oct 23, 2025

- 4 min read

Less than three months after the sweeping devaluation of the Alliance Bank Visa Infinite and Visa Platinum, the noise has died to a whisper.

Promotional pushes have vanished, influencer chatter has evaporated, and on the ground the cards feel MIA. It’s a dramatic reversal for products that, until recently, rode a genuine wave of popularity.

For context, even Maybank’s headline-grabbing miles devaluations last year didn’t trigger an immediate exodus; usage tapered, then collapsed only after a viral Instagram Reel dragged the news into the mainstream.

Alliance’s fall, by contrast, was swift and absolute.

The Tragic Fall

Why did Alliance Bank’s descent happen so fast? Start with positioning.

Alliance has never been one of the market’s “big guns”—if anything, the cards made the bank, not the other way around.

Once the music stopped (i.e., the devaluation landed), cardholders had little reason to stick around when superior alternatives were everywhere.

The killer blow was timing: devaluing your two flagship mass-affluent cards on the same day is akin to throwing your most valuable assets down the drain. Many users didn’t “adjust”—they simply left.

Are Gamers to Blame?

There’s a popular narrative that Alliance’s portfolio was “for gamers” because e-wallet reloads could net roughly 0.53 MPR. That does explain some acquisition, but it doesn’t explain retention—especially after a devaluation.

A niche cohort reloading e-wallets isn’t enough to prop up a mass-market card long term. What we’ve seen instead is mainstream abandonment where ordinary consumers, not just niche optimisers, moved on when the overall value story collapsed.

Where Alliance Bank Lost: The brutal RM60k Battlefield

The RM60,000 annual income segment is the most hotly contested tier in Malaysia for airline miles seekers—and even if you zoom out beyond miles enthusiasts, a huge chunk of earners fall around or just above this bracket. The competition here is ruthless.

Look at the line-up most consumers evaluate: UOB World Card, UOB PRVI Miles, CIMB Visa Infinite—and, formerly, the now-hollow HSBC TravelOne before its income-bar change.

Notice something? None of these cards copy Alliance’s “two-speed” earn model that simply pays different points for local vs overseas.

Yes, Alliance’s 10X overseas headline rate looks attractive on paper, and in raw terms the overseas MPR was compelling. But the incremental upside on a few foreign trips a year doesn’t offset a sea of losses elsewhere—unless you’re abroad half the year and you adore Enrich miles enough to accept the domestic haircut.

Lounge Access Born Out of Wedlock

Perhaps the most baffling part of the newly “revamped” Alliance Bank Visa Infinite lies within its lounge access benefits—or lack thereof.

To give credit where it’s due, the Alliance Bank Visa Infinite technically boasts one of the widest lounge access networks in Malaysia, rivalled only by CIMB and the usual suspects like Priority Pass, DragonPass, and LoungeKey. But that’s about where the compliments end.

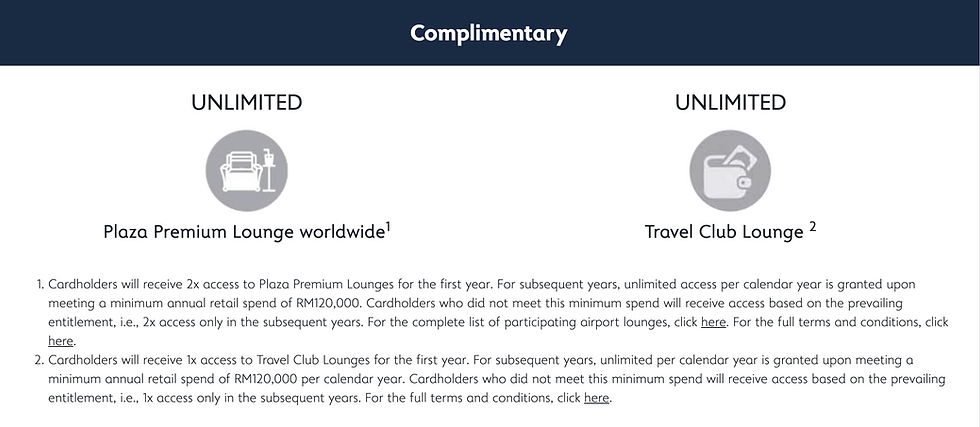

The card offers a laughable 2x Plaza Premium Lounge visits per year and a single visit to Travel Club Lounges—a lounge so underwhelming that most frequent travellers wouldn’t even bother stepping foot inside.

But the real comedy begins with Alliance Bank’s so-called “unlimited lounge access” perk, which unlocks only after you spend RM120,000 a year.

Let’s pause for a moment and think about that. The card’s income requirement is RM60,000 per year, yet you’re expected to spend double your annual income just to enjoy unlimited lounge access. It’s as if Alliance Bank believes Malaysians are so obsessed with lounge access that they’d willingly rack up debt just to sip unlimited free coffee and eat mass-produced nasi lemak in an airport lounge.

Even if someone does have the means to spend RM120,000 a year, why on earth would they pick the Alliance Bank Visa Infinite over far superior cards in that range, such as the CIMB Visa Infinite, which offers better benefits, a more logical structure, and significantly better value?

It’s one of those classic examples of a benefit designed by a team so out of touch with reality that it borders on parody.

Looking Ahead: What’s Left that Still Works

The golden era is over, much like Maybank’s is over in the miles game—except Alliance Bank doesn't have the luxury of being the largest bank in Malaysia so the fallout hurts more. If you insist on extracting the last drops of value, there is one realistic route:

The Alliance Bank Virtual Visa Platinum still earns roughly 0.53 MPR on e-wallet reloads (capped at RM3,000 monthly). If you want to drip-feed Enrich for short-haul ASEAN hops, this remains usable.

Otherwise, the Hong Leong Bank Sutera Visa Platinum offers a cleaner, long-term alternative for Enrich collectors with an unlimited 0.33 MPR on E-wallets, plus 0.33 MPR on convenience stores, pharmacies and major e-commerce platforms.

For most people, the overall utility and predictability beat Alliance’s post-revamp patchwork.

Final Thoughts

Alliance Bank didn’t just tweak earn rates; it detonated its own value proposition and, with it, consumer trust.

When the core mechanics of a card stop making sense—earn structures that don’t match real-world spend, lounge benefits gated behind unrealistic thresholds—customers vote with their wallets. That’s exactly what happened here.

For everyday miles building, move to ecosystems that are proving durable, predictable, and fast to credit—UOB for speed to KrisFlyer/Asia Miles, CIMB for Avios pathways and frequent merchant promos, or Hong Leong Bank for a straightforward Enrich strategy anchored to dining and broad day-to-day spend.

Until then, the Alliance Bank Visa Infinite will remain what it is today: a once-beloved card that lost the plot—and the market—with it. For readers who care about extracting real value, there are better, saner homes for your spend right now.

Thanks for reminding…to cancel it

forgot this card exist before you wrote about it 😅